The Bank of England was widely expected to slightly increase its official bank rate on November 4, but it decided to stick to the all-time low of 0.1%. However, the bank has made it clear that a rise will soon be needed, and the recent increases in mortgage rates indicate that lenders agree. So why the decision to hold off?

The Bank of England is well aware of the distress that higher rates cause for borrowers and, in particular, for the biggest borrower in the land: the UK government. At the current level of national debt, roughly GBP 2trn (USD 2.69trn), every rise in rates by one percentage point pushes up the interest paid by the government on its bonds by GBP 20 billion per year over the long term.

Higher rates also have a dampening effect on the prices of property and financial assets such as shares. Indeed, this is one way in which monetary policy is believed to work: if people feel less wealthy, they spend less and this relieves the pressure on inflation.

On the other hand, what’s bad for borrowers is good for savers. As rates rise, bank deposits will be better rewarded and even the finances of our beleaguered pension funds should begin to look more healthy.

But regardless of who wins and who loses from higher interest rates, inflation is on the rise. The bank does not want to lose credibility by letting it rise too far before tightening monetary policy.

The inflation dilemma

After rising for the past 12 months, UK inflation is currently 3.1%, and the bank expects it could even reach an uncomfortable 5% by early next year – much higher than its 2% target. Yet the bank maintains the view that this higher inflation will turn out to be temporary, arguing that it will fall back as the post-COVID excess demand for goods subsides and supply bottlenecks are worked out. Against that, energy prices are likely to remain higher, driven partly by climate initiatives; and if employers continue to have trouble filling vacancies, higher wages will also tend to push up prices.

The bottom line is that nobody really knows where inflation is heading, so the bank is wrestling with the usual dilemma: does it raise rates now to forestall future inflation, or does it hold rates down to avoid jeopardizing the economic recovery while hoping that inflation will subside by itself? It can’t have it both ways.

Annual inflation 2019-21

This same dilemma is echoed in other countries. In the United States, the position is similarly troubling, with inflation already at 5.4% against a 2% target. Yet the Federal Reserve also continues to insist that the current high inflation is temporary, thereby justifying keeping its official interest rate (the Fed funds rate) near zero.

Yet the Fed is not completely sitting on its hands; it has announced that it will start “tapering” its quantitative easing (QE) programme, in which it is creating USD 120bn a month to buy US government bonds and other financial assets to help prop up the economy. From the middle of November, it will scale this back by USD 15bn each month. This is at least an acknowledgement by the Fed that its excessively stimulatory monetary policy must eventually come to an end.

Back in the UK, the Bank of England has accumulated GBP 800bn of government debt as a result of its own QE asset purchases, designed to stimulate demand particularly since the outbreak of COVID. At some stage, the bank will need to begin offloading this debt.

Its choices of when and how to do this present the bank with arguably an even bigger dilemma than the bank rate, because unwinding QE will drive up yields on bonds – thus directly raising interest costs for the government and all other long-term borrowers.

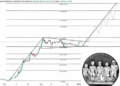

Yields on 10-year UK government bonds

In fact, yields have already started rising after many years of decline (see chart above). This is a sign that investors think that monetary policy needs to become tighter to curb inflation (by raising official rates and reversing QE) – which also explains why mortgage rates have already been rising.

This all confirms that the long era of ever-cheaper finance is finally over. The future will be tougher thanks to higher interest rates, or higher inflation, or both.![]()

This article is republished from The Conversation under a Creative Commons license. Read the original article.

Credit: Source link

{kind=link}