- Dan Morehead is under federal investigation for allegedly misapplying Puerto Rican tax exemptions to classify US$850M+ in profits as tax-free.

- The US Senate Finance Committee is cracking down on wealthy individuals using Puerto Rico’s tax breaks to avoid US taxes, reinforcing that most gains remain taxable.

Pantera Capital founder Dan Morehead is under federal investigation for potential tax law violations following his move to Puerto Rico, a US territory known for its tax incentives.

A letter from Senator Ron Wyden, dated January 9 and obtained by The New York Times, suggests that Morehead may have misapplied tax exemptions available to Puerto Rico residents. Morehead said in a statement:

I believe I acted appropriately with respect to my taxes.

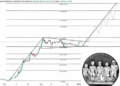

Pantera Capital founder Dan Morehead

Pantera Capital founder Dan MoreheadRelated: Taurus Launches Enterprise-Grade Tokenisation Platform on Solana, Backed by Deutsche Bank

The US Senate Finance Committee (SFC) is examining whether he improperly classified over US$850M (AU$1.33B) in investment profits as exempt from federal taxes.

This comes as the SFC tightens its grip on high-net-worth individuals who relocated to the island to avoid paying US taxes on income sourced outside Puerto Rico.

The letter states that such gains remain taxable under US law and that “In most cases, the majority of the gain is actually U.S. source income, reportable on U.S. tax returns, and subject to U.S. tax.”

Related: Binance’s “CZ” Sparks Meme Coin Frenzy with Dog Name Reveal

Fund Generates Hefty Returns

Pantera Capital was the first US crypto investment fund. In a November 2024 blog post, Morehead noted that its initial investments had grown by more than 130,000%.

Pantera’s Bitcoin Fund, launched in July 2013, reportedly generated returns over 1,000 times its original Bitcoin purchases at US$74 (AU$116) per coin back then. The firm now manages over US$5B (AU$7.86B) in assets, with nearly half its capital invested outside the US.

Morehead’s case is part of a broader crackdown on cryptocurrency tax compliance. In June 2024, the Internal Revenue Service (IRS) introduced new rules requiring third-party tax reporting on US crypto transactions.

In December 2024, the Blockchain Association sued the IRS, arguing that the new regulations are unconstitutional.

Credit: Source link

{kind=link}