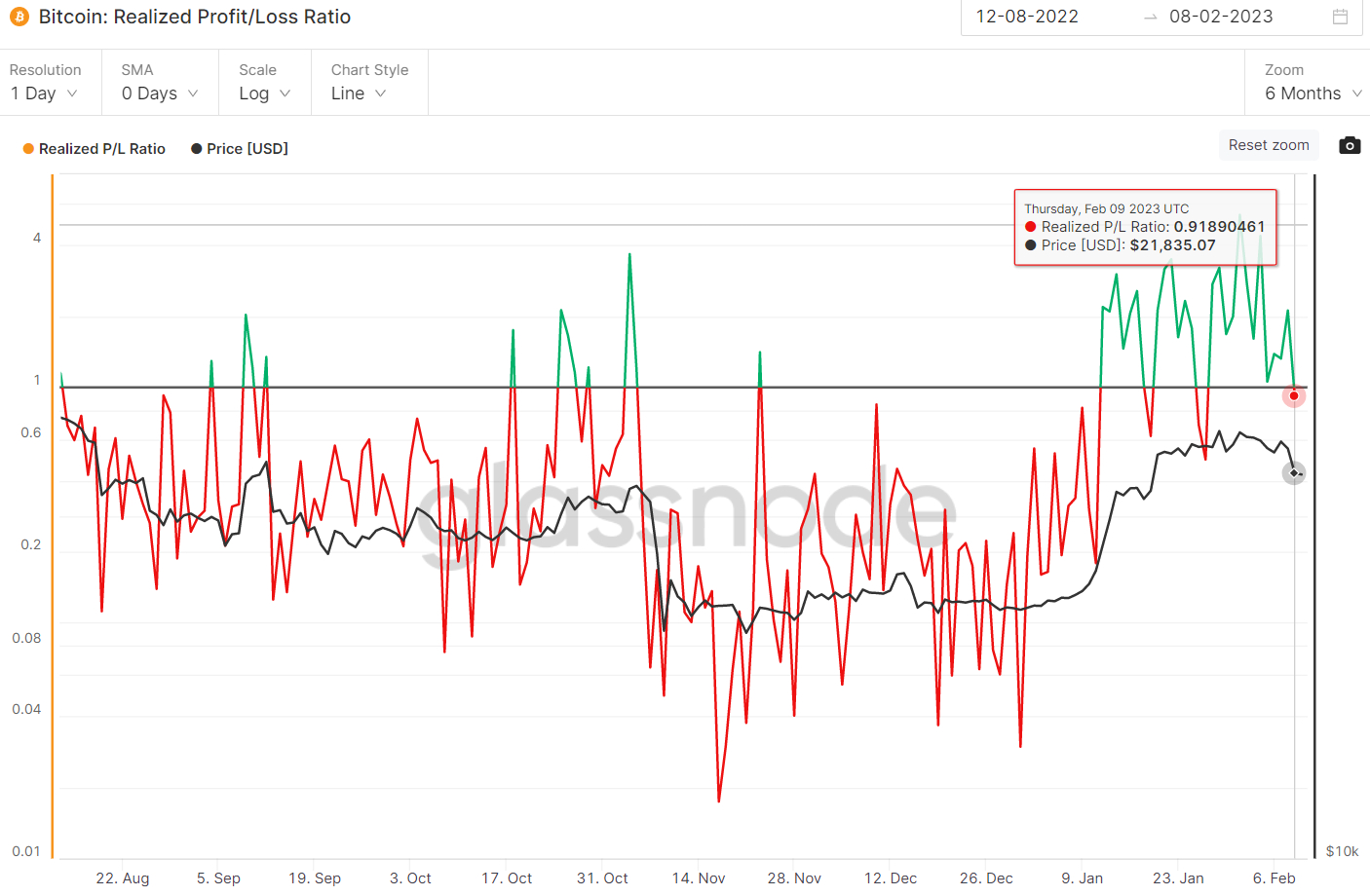

The ratio between all Bitcoins moved at a profit and loss fell below 1 for the first time in more than two weeks on Thursday the 9th of February, according to data from crypto analytics firm Glassnode. The so-called Bitcoin Realized Profit/Loss Ratio fell to 0.9189 as Bitcoin’s price slumped to a new near-three-week low under $22,000 amid concerns about 1) a US regulatory crackdown that is for now focused on US-based crypto staking service providers, but could soon spread to other parts of the industry and 2) concerns that the Fed might end up raising interest rates more than expected this year.

That means that, on Thursday, the Bitcoin market realized a greater proportion of USD-denominated losses than profits. Prior to Thursday’s 5% one-day drop, Bitcoin had already pulled back 5% from its earlier monthly highs in the $24,000s, but the Realized Profit/Loss ratio had remained positive. That indicated that downside was likely a result of profit-taking from those who had bought earlier in the year, prior to/during Bitcoin’s big run-up.

However, the Realized Profit/Loss ratio turning negative on Thursday suggests that a greater proportion of the sell pressure was likely a result of traders who had gone long within the last few weeks being stopped out. Future position liquidation data from crypto derivatives analytics firm coinglass paints a similar picture. Bitcoin long position liquidations spiked to their highest in over three months at $64.6 million on Thursday.

What Next for BTC?

As the week draws to a close, the Bitcoin price is now consolidating just above the key $21,500 resistance-turned-support area and traders are wondering whether all of the short-term “weak hand” investors have been wiped out. Anyone who placed their stop in the low-$22,000s is now surely gone.

But even if the bulk of the short-term speculators who bought in the mid-$22,000s and above are now out of the market, profit taking by those who bought earlier this year under $20,000 could well continue to weigh on prices. If Bitcoin’s price continues to drop this weekend/next week but the Realized Profit/Loss ratio recovers back above 1.0, that would imply increased profit-taking from this cohort.

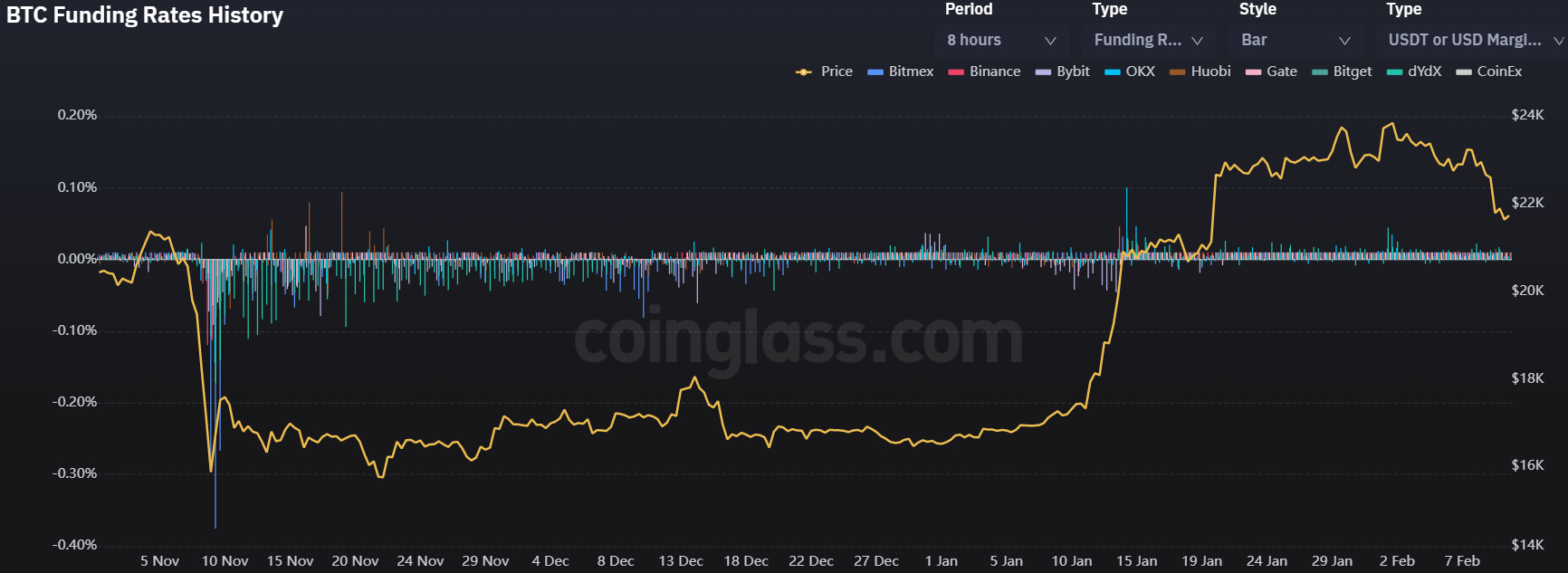

That might arguably be taken as a bearish signal, given it is a show of doubt by potentially longer-term holders in the sustainability of the 2023 rally. But, for now, Bitcoin bulls shouldn’t panic. Coinglass data shows that despite Thursday’s drop, there hasn’t been a shift in Bitcoin leverage funding rates, which remains modestly positive. According to coinglass, “positive funding rates suggest speculators are bullish and long traders are paying funding to short traders”.

While options markets have shifted to position for a slight increased risk of near-term downside over the course of the next seven days, many traders remain confident that the latest pullback isn’t the start of a drop back to 2022 lows. Indeed, options markets are still sending positive signals regarding Bitcoin’s longer-term outlook, as captured by the fact that Bitcoin’s 180-day 25% delta skew remains above zero and close to recent highs.

Given the growing list of on-chain and technical indicators that are all now screaming that the bear market of 2022 is likely over, and the fact that, even if the Fed does do a few extra interest rate hikes, the end of tightening still remains in sight, to expect a positive bias for the year continues to make sense. But if next week’s US Consumer Price Index data delivers an upside surprise, Bitcoin could certainly be in for some more short-term pain.

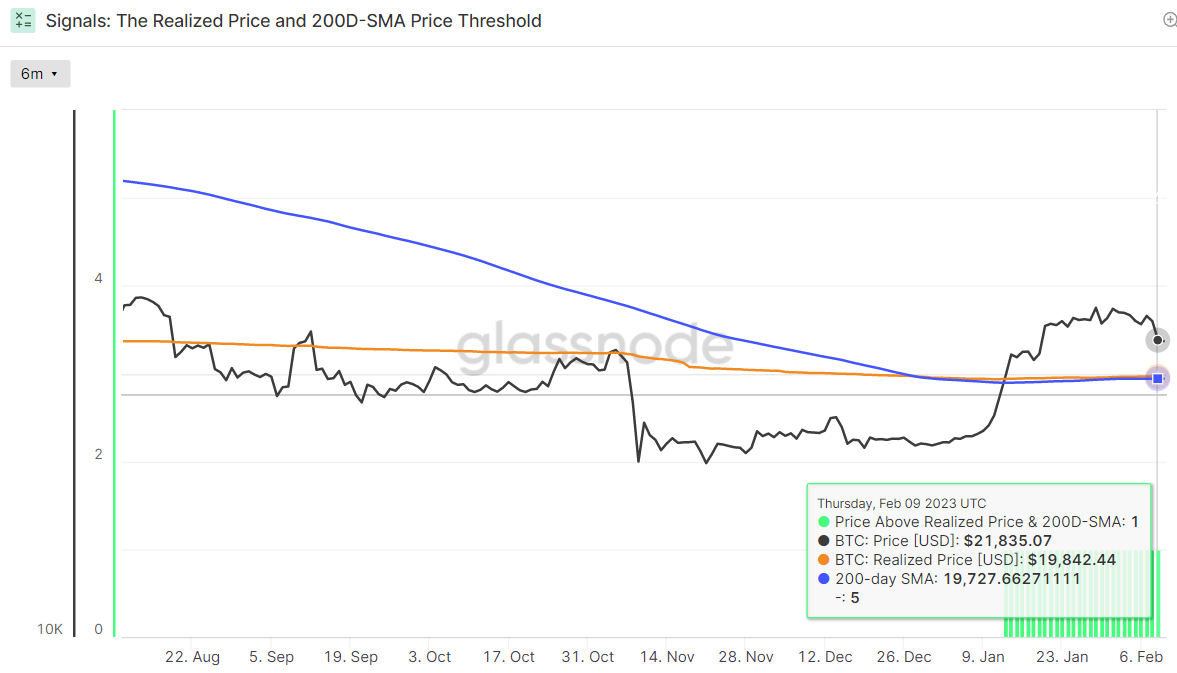

A dip to sub-$20,000 levels could be on the cards, which would likely trigger a fresh stop-run on short-term speculators who went long in the $20,500-$21,500 supply area. However, expect dip-buyers to be waiting eagerly to scoop up a good amount of Bitcoin as it approaches its 200-Day Moving Average and Realized Price, both of which reside in the $19,700/800 area.

Credit: Source link

{kind=link}