- BIS warns that while tokenisation offers cost reductions and streamlined transactions, it raises concerns about governance, legal frameworks, and financial stability.

- The report highlights the uncertainty surrounding how tokenised financial products, such as repurchase agreements, will be treated legally, especially in bankruptcy situations.

- The BIS also noted that tokenisation could disrupt central banks’ roles in payments and financial oversight, requiring careful regulation to mitigate risks.

The Bank for International Settlements (BIS) has issued a report highlighting potential risks associated with the growing trend of tokenisation in traditional finance.

While tokenisation — the process of converting real-world assets (RWA) like property and securities into digital tokens — offers benefits such as cost reduction and streamlined transactions, the BIS is worried about governance, legal frameworks, and financial stability.

Related: Real-World Asset Tokenisation Set for Explosive Growth, Predicts Report

Exploring Tokenisation in Traditional Finance

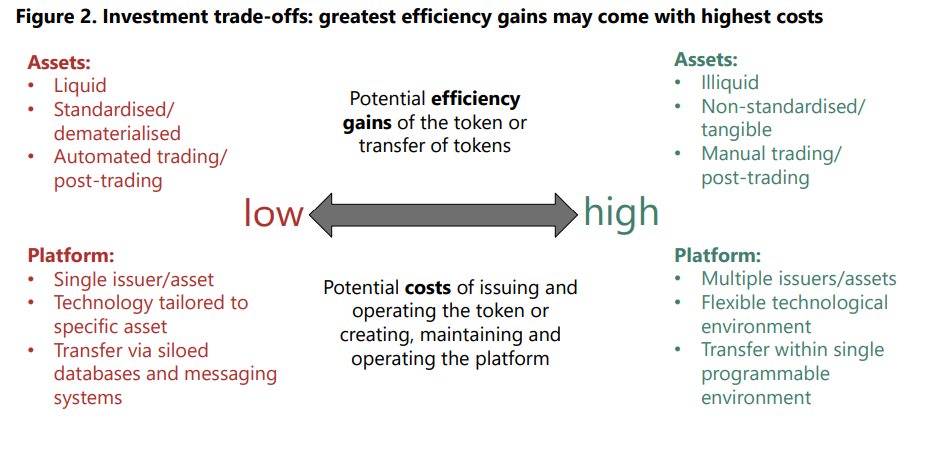

Tokenisation can reshape current market structures by reducing transaction costs and improving settlement efficiency through mechanisms like delivery-versus-payment (DvP) and payment-versus-payment (PvP).

It also breaks down geographical and regulatory barriers. For instance, European investors can invest in American real estate without having to move there, given that the property is tokenised on the blockchain, dividing it into smaller, tradable units, something known as fractional ownership.

However, the fact that it can break regulatory barriers doesn’t mean governments will not impose regulatory challenges, the BIS warned, especially regarding how existing laws apply to tokenised financial products. For instance, it remains unclear whether tokenised repurchase agreements (repos) would receive the same legal protections as traditional repos in bankruptcy proceedings.

Agustín Carstens, General Manager of the BIS, said these technical challenges must be addressed to unlock the full potential of tokenisation:

Tokenisation has significant potential to improve the safety and efficiency of the financial system […] However, tokenisation also poses economic, legal and technical challenges that must be addressed if it is to fulfil its potential.

Agustín Carstens, BIS

Agustín Carstens, BISMoreover, the tokenisation process can be costly, demanding “significant investment and coordination”, the report says.

Tokenisation Could ‘Disrupt Central Banks Roles’

The report also cautions that tokenisation could disrupt central banks’ roles in payments, monetary policy, and financial oversight. Policymakers are encouraged to weigh the trade-offs of using various settlement assets and ensure that private sector tokenisation initiatives are properly regulated to maintain financial stability.

Despite the risks, major financial institutions like Barclays, Citi, and HSBC are pressing forward with tokenisation projects. Trials such as the UK’s Regulated Liability Network (RLN) are testing the feasibility of tokenised deposits and programmable payments.

The market for tokenised RWAs is expected to grow rapidly, with estimates ranging from US$4 trillion (AU$5.98 trillion) to US$30 trillion (AU$44.9 trillion) by the end of the decade.

Related: Chainalysis Report Reveals Asia and Oceania Lead in Global Crypto Adoption

The BIS report concludes that while tokenisation has the potential to revolutionise finance, significant investment and coordination between the public and private sectors are needed to manage risks and unlock their potential.

Credit: Source link

{kind=link}